UnitedHealth’s self-dealing is accelerating

It’s paying itself billions and avoiding federal requirement on health care patient spending

UnitedHealth Group’s internal revenue streams totalled $138 billion in 2023, up more than 25% compared to last year. It’s doing more business with itself than ever before. When its insurance division pays for an enrollee to visit a primary care physician it employs, despite having alternative options with competing practices, one subsidiary is simply reimbursing another.

There are a number of reasons why such transactions, in any industry, could be logical–and are legal. But there are also a number of reasons they could be alarming. Is a company self-selecting, denying others a chance to sell their services? Could a company be providing lower quality services because it’s guaranteeing business to itself? Or could it be avoiding oversight that’s inherent in doing business with other companies? These possibilities are of particular concern in an industry like health care, where quality and affordability are paramount.

It’s difficult to know exactly how much business UnitedHealth, the largest for-profit, vertically-integrated health care company in the country, does with itself. One indicator, though, is the value of the “eliminations” that the company deducts from its revenue in its quarterly earnings reports to investors and regulators. This figure represents the amount of money that Optum generates from “affiliated customers.” Optum, one of two major UnitedHealth subsidiaries, includes physician services, a pharmacy benefit manager (PBM), claims integrity processing, revenue cycle management, and more. [The other is UnitedHealthcare, which provides insurance plans to employers, Medicare and Medicaid members, and others.]

The elimination data appears in UnitedHealth’s quarterly reports like this (taken from its 2023 third-quarter 10-Q):

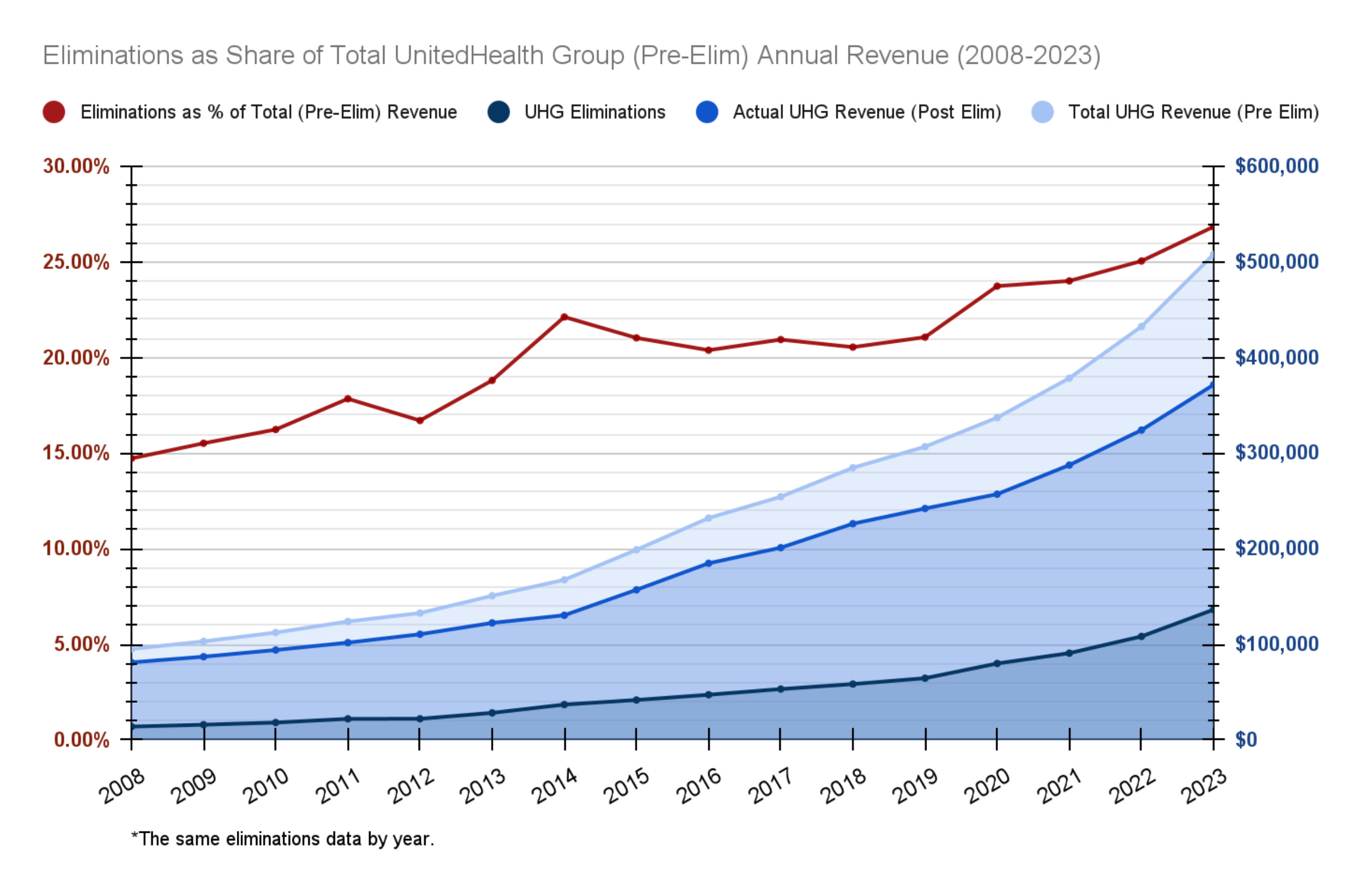

In the above table, UnitedHealth’s financial planners had to subtract the $34.2 billion that Optum made from affiliated customers from the $69.9 billion and $56.7 billion that UnitedHealthcare and Optum made in total (or $126.6 billion combined) to arrive at the final $92.4 billion in actual revenue that the company reported. In other words, 27%, more than one-fourth, of the total pre-elimination business UnitedHealth did in the third quarter of 2023 was just with itself (34.2/126.6). That was a record for the company, according to a new analysis by HEALTH CARE un-covered of its quarterly eliminations dating back to 2008. Today, UnitedHealth released its latest round of earnings, and we can report it set yet another record in the fourth quarter of 2023: $35.9 billion in eliminations, or 27.5% of its revenue (pre-eliminations).

Here’s how that stacks up against UnitedHealth’s quarterly eliminations historically:

The data shows that UnitedHealth’s inter-subsidiary business dealings have been growing as a share of its total revenue over time, almost doubling over 16 years from about 15% in 2008. This means that UnitedHealthcare insurance plans are not only increasingly paying to use Optum’s physicians, PBM, claims integrity processing and revenue cycle management, but that UnitedHealth’s overall growth appears to be dependent on these kinds of internal transactions. And there is no sign that they’re slowing down by looking to send their patients to other medical practices or hiring the services of other businesses.

For comparison, in 2022, Cigna’s interbusiness eliminations made up just 3.7% of its $187.5 billion in total revenue (pre-eliminations). And in 2008, that number was less than .3%. Another competitor, CVS had eliminations that made up 12.3% of its total revenue (pre-eliminations) in 2022. In 2008, it was just 5.7%. In both 2022 and 2008, neither competitor had even half of the eliminations that UnitedHealth did. (These companies have not yet released their 2023 figures.)

There are multiple reasons why UnitedHealth may be increasingly functioning like a closed system. First, Optum is a dominant provider of all these other services. One subdivision, Optum Health, acquired or hired 20,000 physicians over the past year and now has 90,000 on its roster, or about 10% of all doctors in the U.S. Another subdivision, Optum Rx, is the third-largest PBM, a kind of company that comes up with and administers drug benefit plans for insurers, or about 22% of the market. It’s also the fourth-largest pharmacy, with about 7% of the market. And its final major subdivision, Optum Insight, is considered by several market research firms to be among the top health-care analytics providers, especially following its 2022 acquisition of Change Healthcare.

So, it makes sense that as Optum gains more market share performing the kinds of services that an insurer and its members seek, UnitedHealthcare would increasingly end up doing business with Optum.

But Optum’s growth may not be sufficient to explain why eliminations are rising as a share of UnitedHealth revenue. To pull the curtain back, experts have noted that there may be some financial engineering motivating UnitedHealthcare to use Optum vendors rather than independent ones. By steering patients to Optum doctors, for example, UnitedHealthcare avoids the “medical loss ratio” (MLR), the 80-85% of premium revenue that the Affordable Care Act requires health insurers to spend on patient care. This high percentage means UnitedHealthcare doesn’t get to keep as many profits, but its parent company can compensate for that by making sure patients are using Optum doctors rather than external ones.

UnitedHealth’s eliminations, though, were rising before the MLR requirement went into effect. Generally, the obligation that a publicly-traded company like UnitedHealth has to deliver ever-growing profits means there’s an inherent logic behind using UnitedHealthcare to create and sustain markets to guarantee Optum’s success. (Hospitalogy’s Blake Madden included a great discussion on these dynamics in a similar analysis of UnitedHealth’s yearly eliminations back in July.)

What’s strategic for UnitedHealth, though, is not necessarily good for the public interest. Some of Optum’s businesses, for example, function to deny necessary care for patients, like the recently acquired naviHealth, which uses algorithms to determine whether an insurer should cover patients’ post-acute treatment. And according to experts, the loss of opportunities for independent doctors and pharmacies to serve patients, as UnitedHealth and other corporate actors capture more of the market, can result in fewer options and reduced quality of care.

Financial analysts have occasionally asked about UnitedHealth’s elimination data in public calls about the company’s quarterly earnings reports. Executives tend to ignore that UnitedHealthcare is increasingly using Optum and instead insist that Optum is reliant on the business that other insurers provide. During a recent call about the 2023 third-quarter report, when eliminations as a share of total company revenue rose from 26.6% the previous quarter to 27%, Optum Health CEO Amar Desai said: “As we think about growth, of course, UnitedHealthcare is a core partner to us, but we continue to have the strength of our medical groups and physician networks being incredibly attractive to other payers regionally and nationally.”

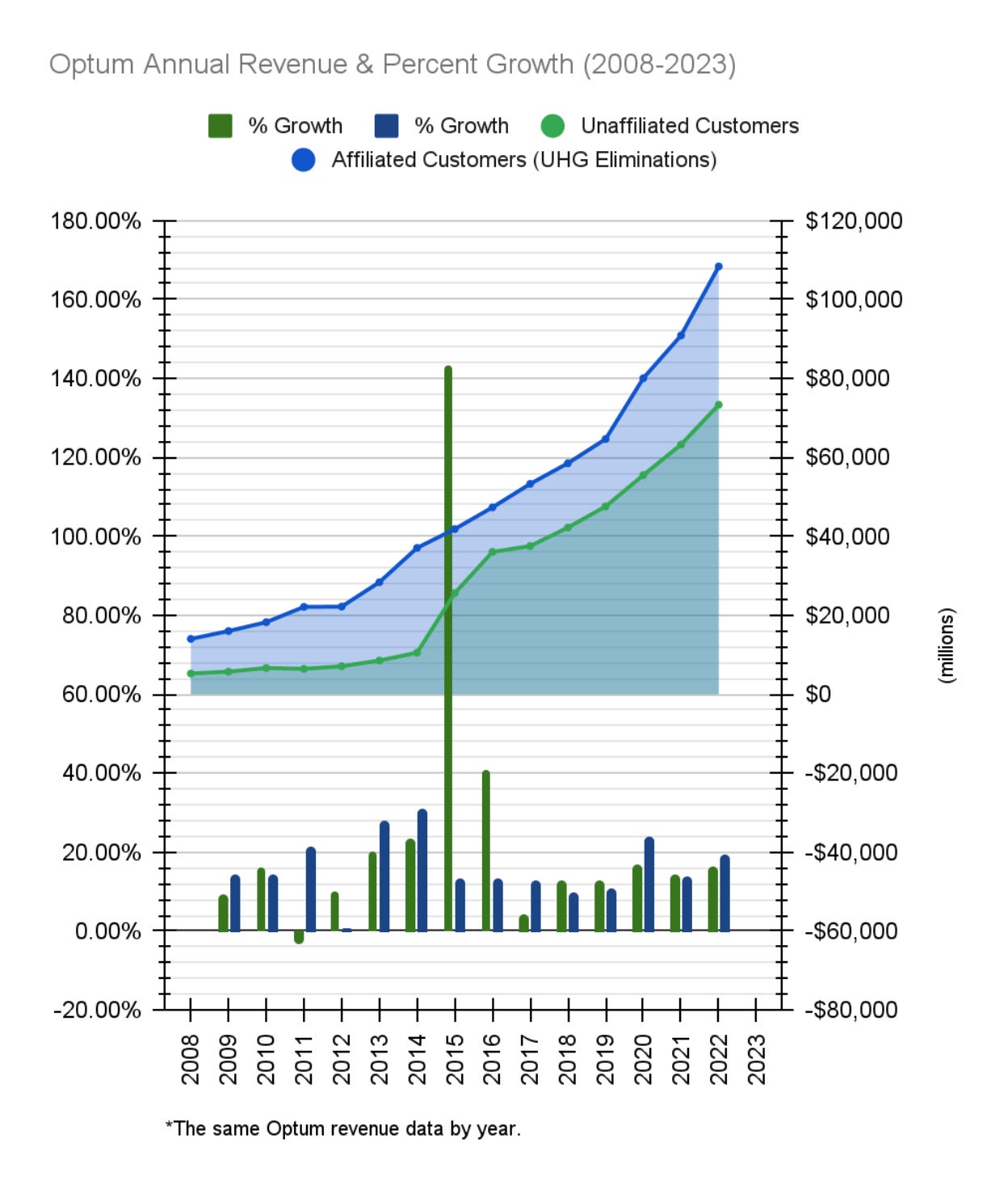

And back in 2015, during a call about UnitedHealth’s second-quarter performance, when eliminations as a share of total company revenue rose from 21.3% the previous quarter to 22.2%, a company executive said: “When you look at it, you’ll actually see that Optum’s overall growth rate is growing at a faster rate than the eliminations, if you will, which suggests that Optum is growing faster externally than they are through the internal business with UnitedHealthcare.”

HEALTH CARE un-covered took a deeper look into this claim, comparing Optum quarterly revenue from affiliated customers (UnitedHealth eliminations) and unaffiliated customers, as well as their growth rates. Here’s what we found:

The executive’s 2015 assertion was, in fact, not true. During the second quarter of 2015, Optum grew faster internally than externally: The money it generated from affiliated customers rose 7.4% from the first quarter, while the money it made from unaffiliated customers rose 1.5%. The third quarter did see a stark reversal, with Optum’s external revenue jumping more than 170%, likely due to its acquisition of what was then the fourth-largest PBM, Catamaran. But several quarters since then have seen Optum revenue rise faster internally than externally, putting into question the notion that its overall growth is more reliant on independent customers than its own.

The data shows that Optum generates the majority of its revenue from UnitedHealthcare, not external insurers. This is not necessarily surprising, given that UnitedHealthcare is a dominant player in the insurance market, like Optum is in its sectors. In fact, UnitedHealthcare is the largest commercial health insurer, with 14% of the market, and the largest Medicare Advantage insurer, with 28% of the market, according to the American Medical Association. So it makes sense that a significant number of customers that Optum serves, and thus makes money from, are insured or owned by UnitedHealthcare. That said, UnitedHealthcare’s large share is still less than half of the overall insurance market, meaning its position is not sufficient to explain why it makes up the majority of Optum’s revenue. This could suggest Optum is giving preferential treatment to UnitedHealthcare. Or that UnitedHealthcare is sending most of its patients to Optum, and that makes up the bulk of Optum’s capacity.

Again, doing business with a subsidiary is not illegal, but when it eliminates choice and can reduce quality, it becomes a problem. There have been a number of lawsuits that call out UnitedHealthcare for dropping providers (making them out of network) and in turn steering patients to Optum care. One suit described it as "lining their own pockets by terminating providers and referring patients to.. a provider owned and controlled by them."

It should be noted, however, that external insurers have certainly grown as a share of Optum’s revenue over time, from 27% in 2008 to 40% in 2022, though this figure has remained relatively flat and even slightly declined since 2016’s 43%. (*Note: The earnings release that UnitedHealth published today does not include information on Optum’s revenue from external insurers. We will update the charts accordingly when UnitedHealth releases its 10-K with the information.)

It raises some questions that Optum’s internal business with UnitedHealthcare is, at times, growing more rapidly than its external business with other insurers. Are Optum’s subdivisions excluding other customers, for example? Is the UnitedHealthcare model evolving to be more dependent on Optum services, such as with the introduction of algorithmic decision-making and changes in the use of what are known as risk-based and fee-based plans? Examining these questions is critical to understanding the evolving nature of UnitedHealth and the health care industry more broadly. They will be considered in future articles.

For access to the data and more charts on our findings, check out our latest post on our new blog site, The Fat.

|

|

|

|

This information is brilliant. I'm hoping that our legislators -- at least those who take their positions seriously, as in "public service" -- are subscribed to Mr. Potter's blog. Out health care delivery system in the US is fundamentally broken.

Too big to fail comes to mind. The 'big gorillas' like United in the Healthcare industry hold a lot of sway over the politics-driven decision makers when it comes to our healthcare. What a mess we've made for ourselves, with an industry that literally makes life and death decisions over our health!