Thanks to reporters at ProPublica and Scripps News, we are learning more about how health insurers cheat patients out of life-saving care

During my debut as a whistleblower before the Senate Commerce Committee back in 2009, I told lawmakers they could not trust Big Insurance to do the right thing for patients or even to follow state and federal laws that had been on the books for years.

Here’s what I told them:

I know from personal experience that members of Congress and the public have good reason to question the honesty and trustworthiness of the insurance industry. Insurers make promises they have no intention of keeping, they flout regulations designed to protect consumers, and they make it nearly impossible to understand — or even to obtain — information we need.

You will not be surprised that nothing has changed. Big insurers continue to break the law with impunity. If anything, they’ve become even more emboldened. They know federal and state regulatory agencies are underfunded and understaffed. Flouting regulations designed to protect consumers is a key way insurers are able to make massive profits for their shareholders and to further enrich their top executives.

Thanks to a recent investigation by reporters at ProPublica in partnership with Scripps News, we are learning more about how insurers cheat patients out of life-saving care by ignoring state laws that mandate coverage for many life-threatening conditions. (As a former Washington correspondent for Scripps-Howard newspapers, I was especially pleased to see that Scripps News is stepping up its coverage of how the business practices of Big Insurance are leading to an untold number of premature deaths and bankrupt families.)

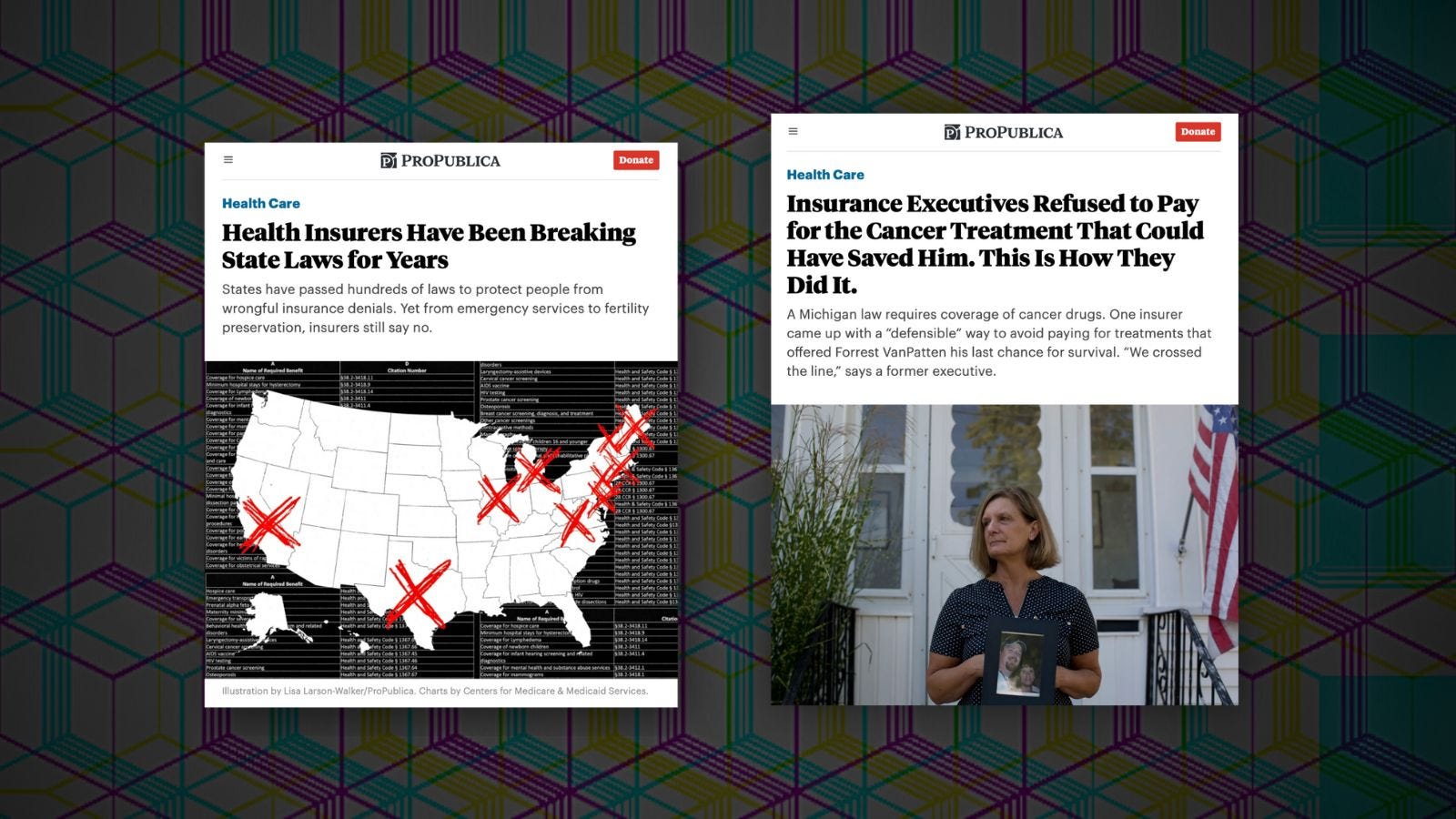

Here’s the headline and subhead of the first in a series of stories ProPublica began publishing last week:

A Michigan law requires coverage of cancer drugs. One insurer came up with a “defensible” way to avoid paying for treatments that offered Forrest VanPatten his last chance for survival. “We crossed the line,” says a former executive.

And here’s the second story in the series, by reporters Maya Miller and Robin Fields, which shows the nationwide scope of insurers’ illegal business practices that are contributing to the deaths of many Americans.

Health Insurers Have Been Breaking State Laws for Years.

States have passed hundreds of laws to protect people from wrongful insurance denials. Yet from emergency services to fertility preservation, insurers still say no.

If nothing else, look at the map included in the story.

Here are excerpts from the first of the reporters’ stories:

Across the country, health insurers are flouting state laws like the one in Michigan, created to guarantee access to critical medical care, ProPublica found. Fed up with insurers saying no too often, state legislators thought they’d solved the problem by passing hundreds of laws spelling out exactly what had to be covered. But companies have continued to dodge bills for pricey treatments, even as industry profits have risen. ProPublica identified dozens of cases in which plans refused to pay for high-stakes treatments or procedures — from emergency surgeries to mammograms — even though laws require insurers to cover them.

Companies can get away with this because the thinly staffed state agencies that oversee many insurers typically don’t open investigations unless patients file complaints. Regulators acknowledge they catch only a fraction of violations. “We are missing things,” said Sebastian Arduengo, an assistant general counsel for Vermont’s insurance department.

In the 34 years since Michigan began to require cancer coverage, regulators there have never cited a company for violating the law…

And this is an excerpt from the second story in the series:

State insurance departments are responsible for enforcing these laws, but many are ill-equipped to do so, researchers, consumer advocates and even some regulators say. These agencies oversee all types of insurance, including plans covering cars, homes and people’s health. Yet they employed less people last year than they did a decade ago. Their first priority is making sure plans remain solvent; protecting consumers from unlawful denials often takes a backseat.

“They just honestly don’t have the resources to do the type of auditing that we would need,” said Sara McMenamin, an associate professor of public health at the University of California, San Diego, who has been studying the implementation of state mandates.

Agencies often don’t investigate health insurance denials unless policyholders or their families complain. But denials can arrive at the worst moments of people’s lives, when they have little energy to wrangle with bureaucracy. People with plans purchased on HealthCare.gov appealed less than 1% of the time, one study found.

Note that those two stories are part of an ongoing series. As you’ll see, the reporters are encouraging patients, doctors, advocates and regulators to reach out to them if they have information the public should know about.

Exactly right, Wendell. State insurance departments are typically somewhere between toothless and impotent, and often deliberately take a "go-along" attitude with the industry they're allegedly regulating. Of course, since the state legislators who control their budget generally want it that way, it's hard to blame them.