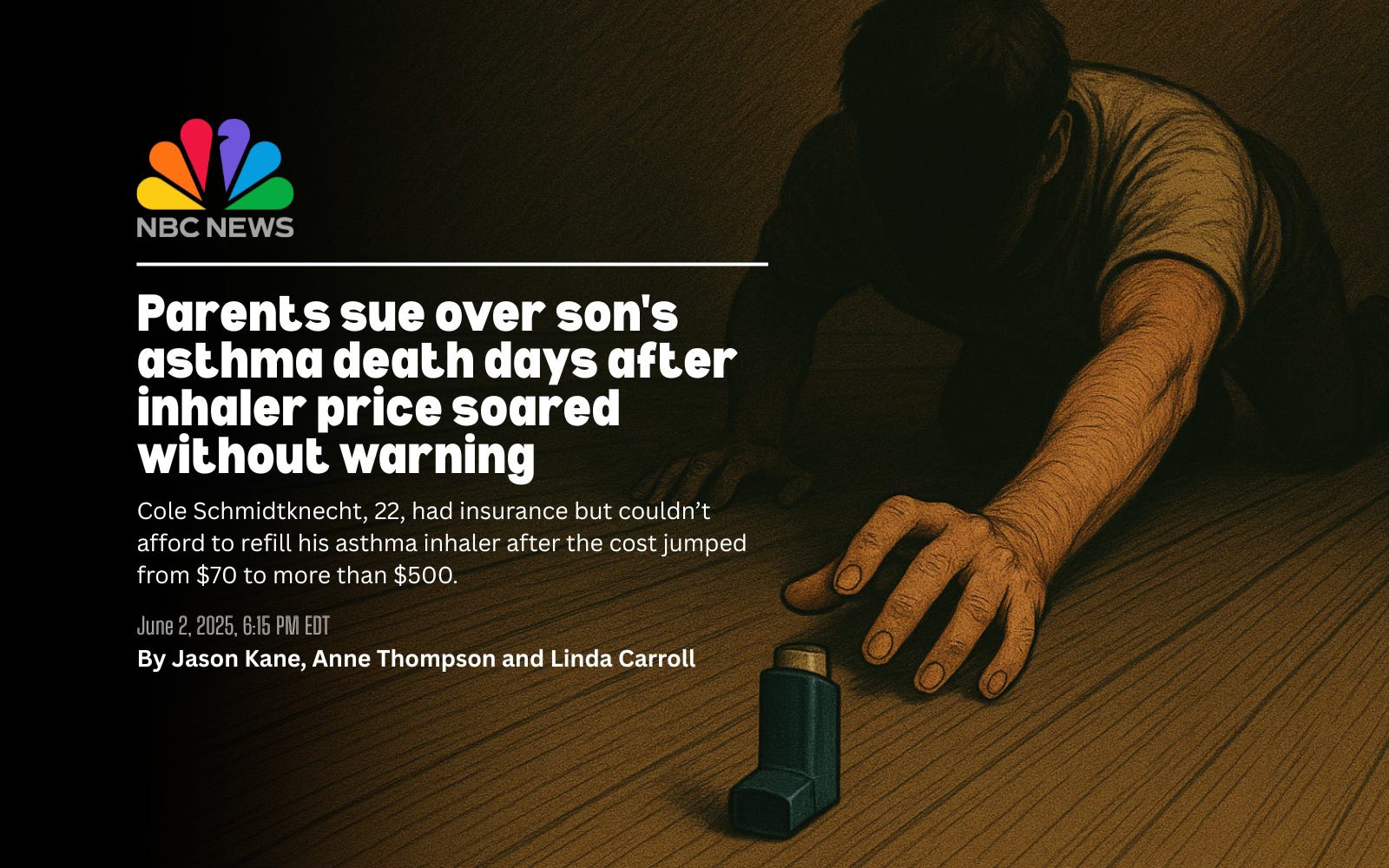

Family Sues UnitedHealth’s Optum Rx and Walgreens Over Son’s Preventable Death

The price of 22-year-old Cole Schmidtknecht’s inhaler jumped from $70 to $500 overnight. Days later, he was gone.

Cole Schmidtknecht should be alive today. He was 22 — young, insured, and doing what he was supposed to do to manage his asthma. But in the blink of an eye, a behind-the-scenes price hike at the pharmacy counter turned deadly. The inhaler Cole had relied on for years — Advair Diskus — suddenly shot up in price from $70 to more than $500. He couldn’t afford it. And five days later, he was gone.

His parents are now suing Optum Rx, the pharmacy benefit manager (PBM) that removed Advair from Cole’s list of covered medications without warning. They’re also suing Walgreens, the pharmacy that didn’t offer affordable alternatives or notify Cole’s doctor, according to the lawsuit reported by NBC News.

This isn’t a one-off story. It’s the logical, predictable outcome of a system designed not around patient care — but around profit.

What Are PBMs and Why Should You Care?

As we’ve written before, PBMs started as simple intermediaries — contracted to negotiate drug prices and lower costs for insurers and employers. But over time, they’ve mutated and vertically integrated with insurance companies that also control physician practices, patient data collection and government contracting – becoming arguably the most powerful and opaque players in American health care.

Today, three massive corporations — CVS Health (through Caremark), Cigna (through Express Scripts), and UnitedHealth Group (through Optum Rx) — control 80% of the PBM market. That level of consolidation has enabled them to quietly inflate the cost of medications for Americans, steer patients to their affiliated pharmacies, and reap rebates and fees at nearly every step of the drug supply chain.

And crucially: Patients rarely know they’re dealing with a PBM at all. But PBMs are the enormously profitable middlemen that not only determine whether your medication will be covered but also how much you’ll have to pay out of your own pocket – often hundreds and sometimes thousands of dollars – even if it is covered.

What Happened to Cole

Cole had insurance. He had a prescription. What he didn’t have was any notice. According to his parents’ lawsuit, Cole was not told his medication would no longer be covered, and his doctor wasn’t notified. And at the pharmacy counter, the lawsuit contends, he was offered only a rescue inhaler — used after an asthma attack starts — not the preventative medicine that could have saved his life.

In a motion to dismiss the case, Optum Rx expressed “sympathies” and argued that federal law bars the case from proceeding in state court. The company also claimed that three other inhalers were available and that its “system” instructed Walgreens to inform Cole’s doctor. Walgreens, for its part, cited privacy and said pharmacy staff generally work with insurers and prescribers to resolve coverage issues.

But that system failed Cole. And it may be failing millions of others in less visible ways.

PBMs Operate With Dangerous Incentive

While Schmidtknecht’s story is tragic and deplorable, NBC News should be commended for sharing it with the rest of us. Americans need to hear stories like this. When we walk up to the pharmacy counter and learn that the medications we’ve been taking for years are suddenly vastly more expensive or not covered at all anymore, we need to know who is responsible, and more often than not it is big health insurance companies and the pharmacy benefit managers they own.

In Cole’s case, his inhaler might have become less profitable for Optum Rx and consequently dropped, without notice to patients, from its list of preferred covered drugs, called a formulary.

PBMs determine which drugs make it onto an insurance plan’s formulary. Drugmakers pay PBMs rebates to secure a good spot on that list. Generally, the more favorable the placement, the higher the rebate. And the bigger the rebate, the more money the PBM (and often its health insurance companies that own them) pocket.

These rebates are rarely passed on to patients. Instead, the higher the list price of the drug, the more room there is for a juicy rebate — and the more incentive PBMs have to prioritize expensive medications. As Gerard Anderson of Johns Hopkins told NBC, PBMs “are looking for the drug that makes them the most money.”

Maintaining Their Profitable Status Quo

A great example of how PBMs preserve their profit machine is through the industry-funded trade group Pharmaceutical Care Management Association (PCMA). Bankrolled by insurance giants like CVS, Cigna, and UnitedHealth, PCMA is currently blanketing Washington, D.C. with ads portraying PBMs as drug price heroes. That’s because members of Congress are catching on to how PBMs really work.

As a result, growing numbers of both Democrats and Republicans are supporting legislation to outlaw many of PBMs’ business practices. What the ads don’t mention is that these PBMs are owned by the very companies (big insurers) and their trade groups that are trying to block reform.

The reason is simple: being a drug middleman has become more profitable than selling insurance. CVS’s Caremark division generates more revenue than Aetna or even CVS’s nearly 10,000 retail stores. Cigna’s Express Scripts division is far bigger and more profitable than its insurance operations. That’s why those companies are pouring millions into lobbying and PR — not to help patients, but to protect a business model that denies coverage, limits drug choices and inflates costs.

And here’s the kicker: you’re paying for it. These campaigns are funded by your premiums and taxes.

Some in Washington Are Taking Action

Yet even as your hard-earned money is paying for those ads flooding the airwaves in D.C., a bipartisan group of lawmakers is pushing back, introducing bills to bring long-overdue transparency and accountability to PBMs and to reduce the amount of money they force Americans to shell out at the pharmacy counter.

One of those lawmakers, Rep. Jake Auchincloss (D-Mass.), honored Schmidtknecht’s life on the House floor by telling his story. He also reminded his colleagues of the Federal Trade Commission’s damning report on PBM business practices and what Washington can do to stop tragedies like Schmidtknecht’s from happening again.

“No family should suffer the loss of a child to PBM greed,” Auchincloss said. “This is not a partisan issue. Cole had his whole life ahead of him. Because Cole was forced to choose between paying his rent or shelling out hundreds of dollars to cover his medication out-of-pocket for a drug that did not need to be that expensive, his family is without their loved one.”

Whether the momentum from Auchincloss, his bill co-sponsors, including Rep. Diana Harshbarger (R-Tenn.) and other members of Congress continues will depend on whether Washington listens to the American people — or the middlemen with the biggest checkbooks.

It’s very complicated even for a health professional like myself. I spend hours each year trying to figure out the best formulary and pharmacy prices and coverage for my wife and myself on Medicare Part D meds. It’s meant to be totally confusing to us as BPM’s and insurers sit in smoked filled rooms looking to boost bottom line profits and no concern on effect of their customers. It is criminal.

I have an inhaler that the generic form costs 3x as much as the brand name. And the generics are mostly now in the hands of big pharmaceuticals and they have split costs of generics into two tiers, go figure! Our government should never have allowed these companies to write the legislation, bribe our lawmakers, deny care that is needed, and pass rules that promised no negotiations on drug pricing for years.

It is time seriously for a one payer universal healthcare system in this country. First the people need to unite and rid government of corrupted politicians and it is a relief at least to see some now “opening their eyes” to this disaster.

This is tragic and easily preventable even within the current system by requiring PBM's and insurers to provide adequate notice regarding formulary changes and to continue to cover current drugs at prior rates for a period of time after a formulary change. How about if formularies can't change to drop scripts mid year at all or at least have to continue to cover dropped drugs for those who are currently taking them through the end of the contract term? When you enroll in a health insurance plan, you have a contract for services and choose a plan based in part on the prescription drug list as it is when you enroll. However, if the insurance company wants to change the formulary a month later to drop your needed scripts, they can. What's worse is that a formulary change dropping a necessary lifesaving drug is not a qualifying event to allow you to change plans. The same is true for provider network changes mid year. It's nonsense.