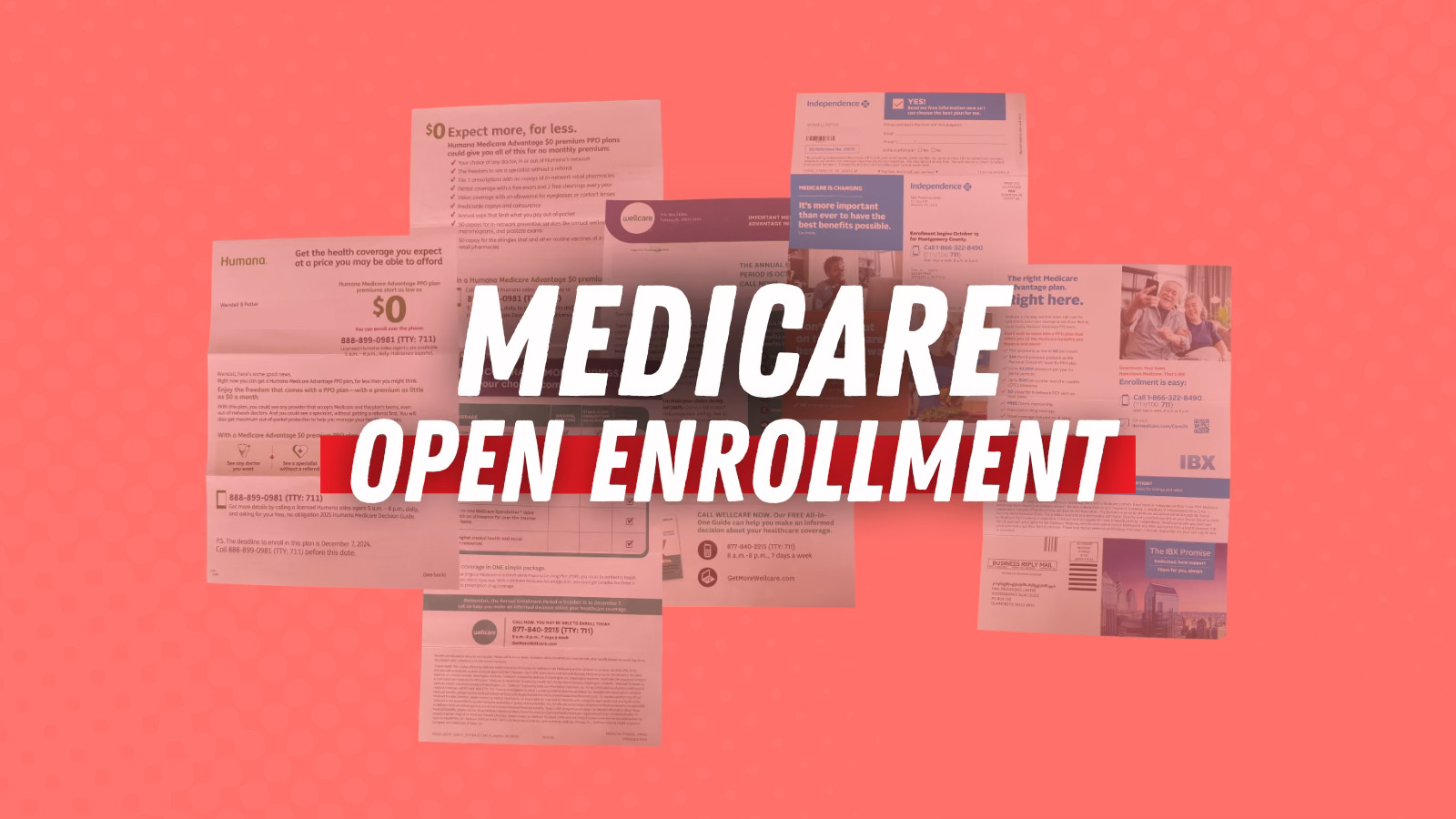

Big Health Insurers Have Begun Their Medicare Advantage Blitz

Something is starting today that once again will set off an enormous transfer of wealth from U.S. taxpayers to a handful of the world’s largest corporations – the ones that are the intrusive middlemen in our health care system.

It is something that does not even need to exist, but because it does, an untold number of seniors and people with disabilities will learn when it’s too late that they were sold a bill of goods, that what they were told was an advantage came with many hidden, life-threatening disadvantages.

I’m talking about Medicare “open enrollment” an eight-week period when Americans eligible for Medicare benefits can choose to enroll – or stay enrolled – in original or traditional Medicare or choose among a bewildering array of private health plans that the federal government allows Big Insurance to market as “Medicare Advantage.” What those seniors and people with disabilities are never told is that all those plans come with hidden landmines, and most of them are owned by just three huge New York Stock Exchange mega-corporations – UnitedHealth Group, CVS/Aetna and Humana.

This year, those three corporations, which are in business first and foremost to make money for their shareholders and top executives, captured 86% of the 1.7 million new Medicare Advantage enrollees. (Captured is the appropriate word, as you’ll learn shortly.) Those three giants pulled this off because the federal government continues to allow them and other big insurers to spend billions of our money on misleading advertising campaigns that intentionally omit crucial information. The feds have permitted Big Insurance to get away with this deception for two decades and as a tragic consequence, more than half of Americans eligible for Medicare benefits are now enrolled in these private plans.

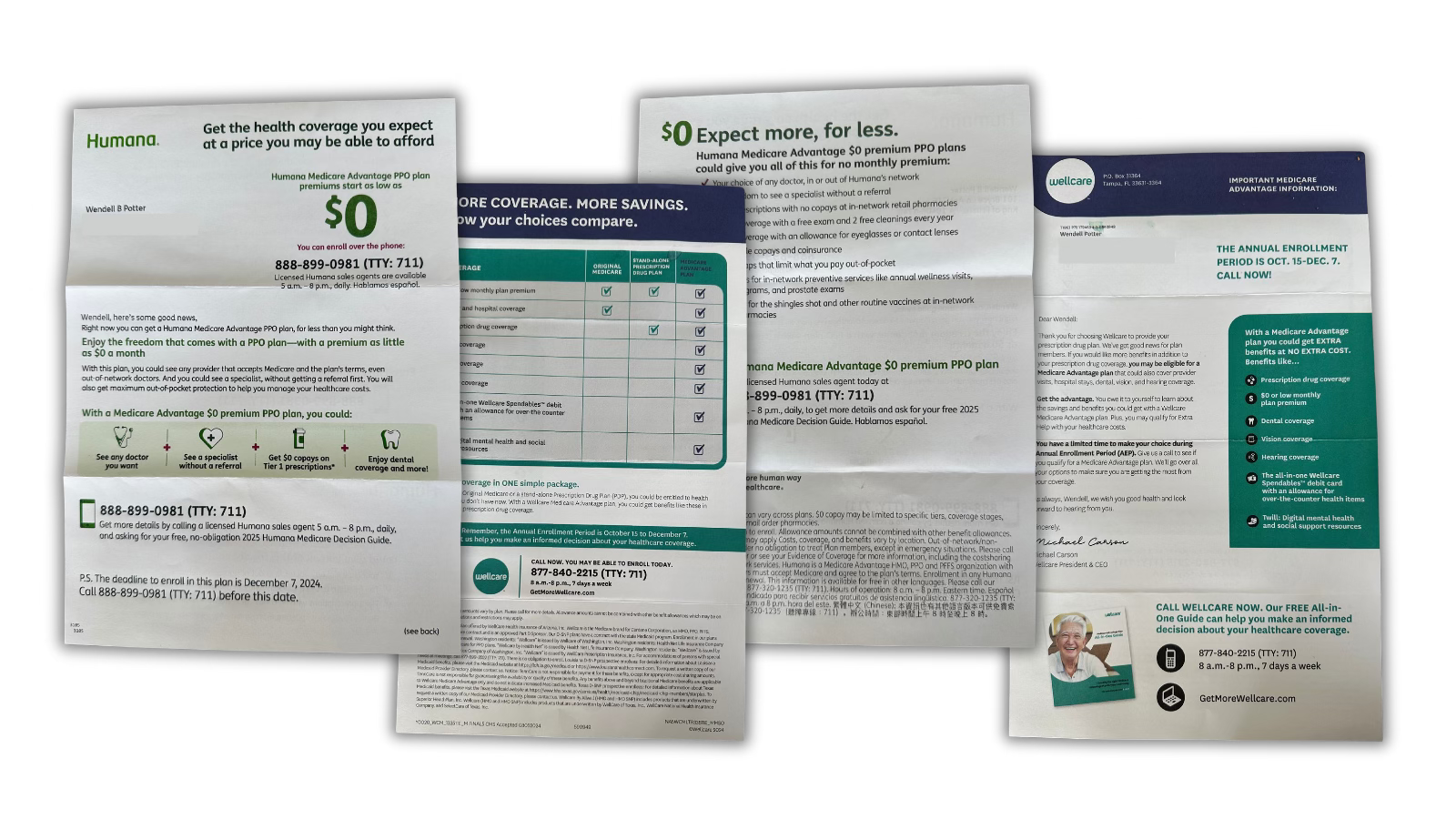

This year’s campaign of deception started in earnest last week. On Friday alone, I got three Medicare Advantage solicitations in the mail that promised me $0 premiums and EXTRA benefits at NO EXTRA COST. It sounds too good to be true and it certainly is, but Big Insurance knows how to sell snake oil. I know that every mail delivery for the next eight weeks will bring more snake oil ads and that we will all see Medicare Advantage commercials countless times whenever we turn on our TVs or scroll through our social media feeds. You can be certain that every one of them will emphasize additional benefits but purposely omit any mention of the following details, any one of which could mean the difference between life and death:

Delays and denials – Unlike traditional Medicare, private Medicare Advantage insurers often overrule patients’ physicians and refuse to pay for medically necessary care. You don’t have to take my word for it because it has been documented by the federal government’s Office of Inspector General and other agencies. Insurers maintain a long list of tests, treatments and medications that require “prior authorization,” meaning doctors have to ask Medicare Advantage insurers for permission in advance before treating their patients. Prior authorization is almost never used in traditional Medicare.

Inadequate provider networks – Private Medicare Advantage plans maintain proprietary and often very limited “networks” of doctors, hospitals and labs and typically refuse to cover care by providers that are not included in those networks. Networks don’t even exist in traditional Medicare. Almost all U.S. doctors and hospitals participate in traditional Medicare.

Potentially high out-of-pocket expenses – If you’re in a Medicare Advantage plan, especially a Medicare Advantage HMO, you could be on the hook for thousands of dollars out of your own pocket if you go to a doctor or hospital that’s not in your insurer’s network. In some counties, Medicare Advantage plans limit your access to doctors and hospitals who are in your county of residence. If you want to go to a specialist or center of excellence in another part of the country or even across the county line, you better have a lot of money in the bank.

Entrapment – Once you’re lured into a Medicare Advantage plan, good luck being able to escape the Medicare Advantage world – ever. While your Medicare Advantage insurer can decide to leave your county whenever it wants – and Medicare Advantage insurers plan to stop serving hundreds of counties in 2025 – you will have a hard time getting into traditional Medicare and buying a Medicare supplement policy to cover your out-of-pocket expenses. You can buy a Medicare supplement policy without going through medical underwriting during your first six months of eligibility for Medicare benefits. But if you enroll in a Medicare Advantage plan and miss that window, you likely will have a hard time finding an affordable supplemental plan, especially if you have any medical issues or “pre-existing conditions.”

When was the last time you heard any mention of those landmines in any of the Medicare Advantage ads that always flood the airways and mailboxes this time of year? Did you ever hear Medicare Advantage shills Joe Namath or JJ Walker utter a word about them? Insurers purposely obscure those vital details because they know that if seniors are aware of them, they’ll be less likely to fall for the Medicare Advantage scam, and they’ll be less likely to be overpaid – yes overpaid – to the tune of $140 billion a year by Uncle Sam, which, incredibly, seems to have been just as hoodwinked over the past two decades as most of America’s seniors.

I hold members of Congress of both parties responsible for this heist of traditional Medicare. For years they have been looking the other way as they accept campaign donations from these corporations’ executives and political action committees.

But I also hold the media responsible. When was the last time you read, heard or saw a story that provided the whole truth about private Medicare Advantage plans? If you see anything at all in the media, it likely will be like this one from Philadelphia’s WHYY, a PBS and NPR affiliate, no less. Reporters, sadly, have also been hoodwinked or just don’t know better. Either that or the people who own the media outlets where they work have become too hooked on the bonanza of Medicare Advantage advertising money that starts flowing their way this time of year.

Thank you for this very good wake-up call for many. Great summary article. I have so many family who always tell me I should change from Medicare to MA where you pay nothing and get "free stuff". They don't understand why I have to pay an out of pocket deductible of 200 some odd bucks every year. Fortunately I had a very good big brother 2 years older than me that set me straight on the hoax when I turned 65.. Unfortunately he died of cancer 2 years ago. But he told me to NEVER go with MA plan, as almost all of his cancer treatments were covered by Medicare and his supplement, whereas they would not be approved if he had MA, and he wouldn't have been able to get back into traditional Medicare since he had cancer. It is shameful that this even exists. You pay into Medicare insurance your whole working life so it will be there when you need it and the greedy corps want to take your health coverage away and give you free band-aids and diapers every month!

Part c Medicare disadvantages only exist with corporate welfare. This welfare (taxpayer dollars) is mostly given to private for profit health insurance companies with Republican support.

I’m noticing the corporate welfare scam is expanding to giving Medicaid taxpayer dollars to private for profit health insurance companies.

All This money must go to providers and communities that actually care for our health.