After missing mid-year financial expectations, here are the ways big health insurers are going to get back into Wall Street's good graces

Hint: it will be at the expense of patients and taxpayers.

Last week, I wrote that the big for-profit insurers made more than $40 billion in profits during the first six months of this year but that Wall Street doesn’t consider that nearly enough. Investors have been shifting money away from those companies, which, I can assure you, has set off alarm bells in the C-Suite.

Because top executives’ compensation is tied to meeting specific financial metrics, including shareholders’ return on investment, the CEOs are especially motivated to right the ship and reduce the percentage of revenues their companies pay out in claims to provider groups and facilities the companies don’t own. You can be certain they’ll be pulling all the levers they can think of.

I would be surprised if some of them haven’t already called in McKinsey & Co. or another big consulting firm to look under the hood. (When I worked in the industry, the chief financial officer of one of my employers had McKinsey on a $50,000-a-month retainer.) But with the stock price falling at all of the companies while the Dow and other Wall Street indices are humming along, the consultants will be called in for a special assignment beyond any retainer. They’ll do a deep dive into the companies’ operating and staff divisions and develop recommendations to “streamline” operations, cut expenses and reallocate resources.

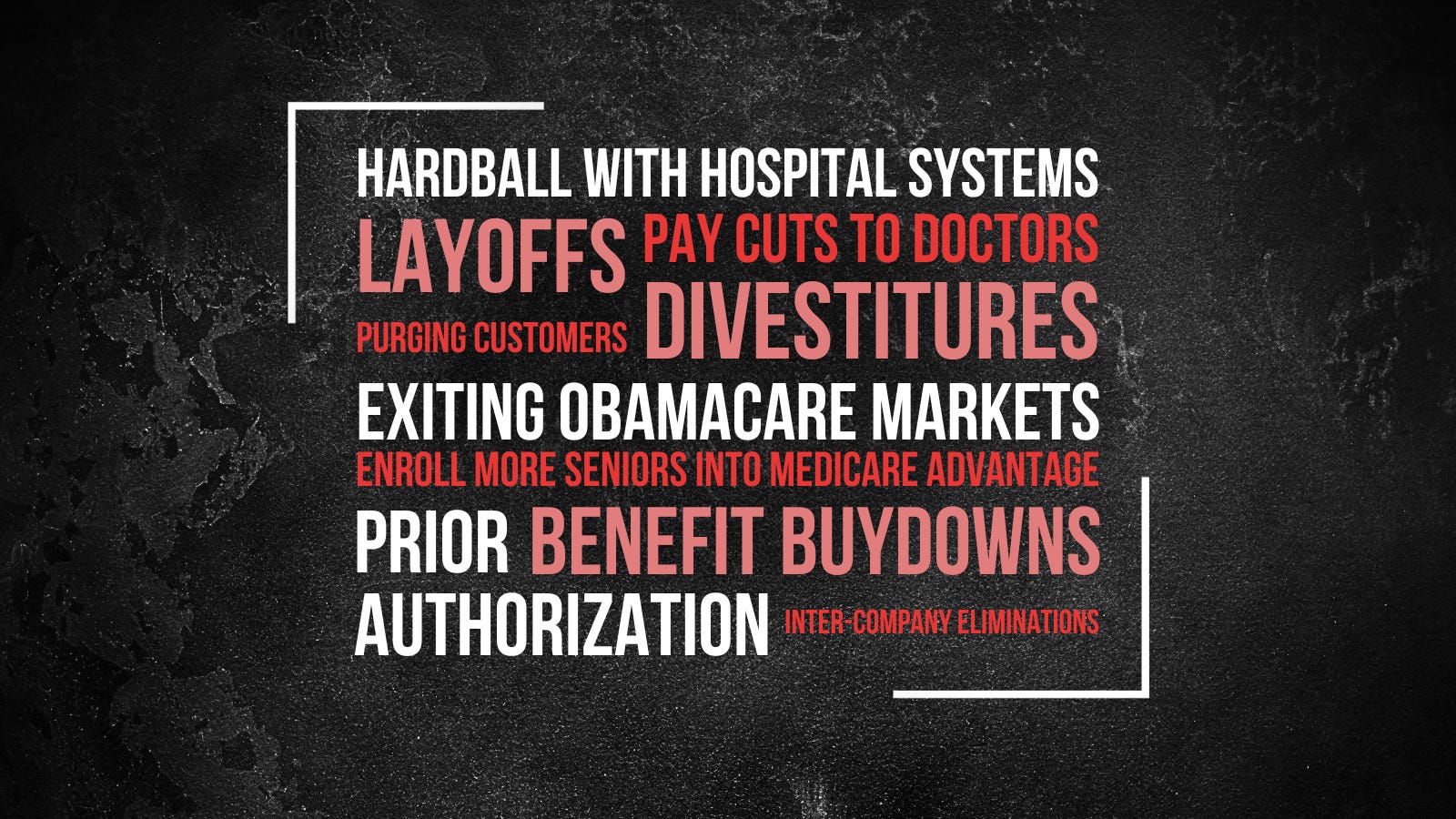

Here are some things to expect in the coming weeks and months at these companies:

Increased hardball with hospital systems: As I’ve reported, Elevance/Anthem, which owns several for-profit Blue Cross plans around the country, is in a protracted dispute with Bon Secours Mercy Health, a hospital system in Ohio and Virginia, over Medicaid and Medicare Advantage reimbursements. Earlier this month, BSMH sued Elevance/Anthem for $93 million in unpaid and disputed claims. The suit claims that Elevance/Anthem’s audits are a “bad faith attempt to bludgeon BSMH Virginia into submission in the contract negotiations, as opposed to a good faith exercise of Anthem’s discretion.”

The dispute between the two parties has attracted considerable media attention, but there are many others across the country. Modern Healthcare reports that so far this year, 49 provider-payer contracting disputes have become public, compared to only 20 through August 2022.

Modern Healthcare is also reporting that many rural hospitals, which typically operate on thin margins, are considering withdrawing from Medicare Advantage networks operated by big insurers because their payments are increasingly inadequate.

Take it or leave it pay cuts to doctors: Just as the pandemic was reaching the United States in early 2020, UnitedHealth Group sent letters to numerous physician groups demanding pay cuts of up to 60%. If the doctors — many of whom were on the front lines trying to keep Covid patients alive — refused, they’d be kicked out of UnitedHealth’s provider network. UnitedHealth rescinded or postponed some of those planned cuts temporarily, but physicians should expect to see those demands again from big insurers.

Layoffs: I know from personal experience that when McKinsey shows up, layoffs are almost always inevitable. Job security for many employees goes out the window. I had to lay off members of my own staff over the years because of the “restructurings” and downsizing McKinsey recommended.

Sure enough, late last month, CVS/Aetna told regulators in eight states that it would eliminate about 5,000 position — even as the company made additional acquisitions, including paying $8 billion for Signify Health, a nationwide network of 10,000 clinicians, and $10 billion for Oak Street Health, a primary care company.

Divestitures: Speaking of CVS/Aetna, I’ve seen reports that investors are questioning the company’s “transformation” efforts, especially in light of the fact that the company’s shares have been down more than 25% since the first of the year. When Wall Street financial analysts signal dissatisfaction with the performance of a company’s operating divisions, the CEO and other executives will assess which operations have become a drain on earnings or are not working synergistically with other and more profitable divisions.

Big insurers are like chameleons, constantly recasting themselves based on Wall Street’s whims. When I joined Cigna in 1993, the company was a large multi-line insurer with a property and casualty division, an individual insurance business, a reinsurance division and a financial services company. Aetna had similar lines of business back then. Both companies shed those operations at the behest of investors and analysts to focus exclusively on health care.

Exiting some Obamacare markets: When the Affordable Care Act marketplaces became active in 2014, most insurers rushed in, and many, the big ones in particular, quickly rushed out. They couldn’t make enough money fast enough to satisfy Wall Street. Since then, the government has increased subsidies (at least temporarily) to help people afford their premiums and out-of-pocket obligations, and many insurers, smelling higher profits, have returned. However, this marketplace can be volatile. Cigna announced last month it is exiting some of the Obamacare markets it had recently entered.

Redoubled efforts to enroll more seniors into Medicare Advantage: Insurers have learned that the federal government is a much more generous customer than the nation’s employers, who once were the primary source of insurers’ revenues and profits. When looking at 2021 data, Kaiser Family Foundation researchers found that “Medicare Advantage insurers reported gross margins averaging $1,730 per enrollee, at least double the margins reported by insurers in the individual/non-group market ($745), the fully insured group/employer market ($689), and the Medicaid managed care market ($768).

Purging customers: The Affordable Care Act makes it illegal for insurers to refuse to sell coverage to people with pre-existing conditions or to charge them more based on their health, but it doesn’t stop them from making premiums unaffordable. Insurers learned long ago that a way to drive away unprofitable individual and small-business customers is to jack up the rates so high those customers will leave. This is known as purging in the health-insurance business. Cigna and other insurers are planning double-digit premium increases for many of those customers in 2024 to boost profits. Cigna’s chief financial officer told investors last month that, “We are likely to have fewer customers in the individual exchange business in 2024 relative to where we are in 2023.” Getting rid of some of those people, he said, should increase the company’s profit margin.

Aggressive use of prior authorization: Federal investigators found in July that some of the big insurers make much more aggressive use of prior authorization in Medicare Advantage and Medicaid than in their commercial health plans, meaning they are refusing to cover the cost of care for many seniors and low-income Americans to boost profits. Doctors have complained for years that insurers are increasingly refusing to pay for care their patients need, regardless of plan type. In the face of congressional scrutiny, Cigna, UnitedHealth and some other companies recently announced they will reduce the number of treatments requiring advanced approval, but don’t be surprised if that applies to a small percentage of patients — and primarily patients receiving care from doctors they employ or who work in clinics and other facilities the insurers own.

Benefit buydowns: An age-old trick insurers have used for decades to improve profit margins is to reduce the value of their health benefit plans while they also increase premiums. Behind closed doors, this is called “benefit buydown.” It manifests in many ways, including making health-plan enrollees pay more out of their own pockets before the coverage kicks in, removing doctors and hospitals from their provider networks, increasing prior-authorization requirements, and refusing to pay claims after medical care has been provided. Cigna reportedly used a software program to reject more than 300,000 requests for payment over two months in 2022. Lawyers in California have filed a class-action lawsuit against the company, claiming it uses an algorithm to deny claims en masse and without human review.

Increase in inter-company eliminations: The ACA requires insurers to pay 80-85% of revenues on patient care. If they spend less than that, they have to send rebate checks to their customers. But the big companies that have moved swiftly into health care delivery have found they can circumvent that requirement — and congressional intent — by paying themselves. The ACA requirement doesn’t apply to health care providers, so UnitedHealth, Cigna and CVS/Aetna in particular are steering their health-plan enrollees to care delivery entities they own. UnitedHealth, which employs more than 70,000 doctors, is clearly the pack leader. During the first half of this year, UnitedHealth categorized $66 billion as “eliminations.” That amounted to 25% of total revenues.

Bottom line: Expect to pay more for your health insurance AND your health care next year — if you can get it at all — to make Wall Street financial analysts and investors (including those in the C-Suite) a little happier and richer.

It appears its time for the US to develop and adopt a universal, national plan that does not involve Wall Street oversight. The US is the only industrialized country that does not have a national plan. Think how much it will save, having the same coding and benefits for all, allowing us to go to any hosptal and not worry about coverage, allowing us to know that all policies have the same benefits, and allowing us to eliminate the greed of Wall Street and insurance companies.

Optum

FSA

Money grab

Any excuse to deny payment directly to physicians and hospitals.