A 50-Year-Old Federal Law Makes It Nearly Impossible to Hold Big Insurance Accountable. I Testified at The Department of Labor About It.

Fifty years ago this month, the Employee Retirement Income Security Act (ERISA) was signed into law with the promise of safeguarding employee benefits. What started as a well-intentioned attempt to protect workers’ health and retirement benefits has since become a shield for the health insurance industry’s most harmful practices. This legal loophole has been a goldmine for the insurance industry, which has successfully lobbied to keep ERISA intact for decades, all while countless patients are left to suffer from decisions made in boardrooms, not doctors’ offices.

ERISA was designed to make it easier for employers, especially those with a national workforce, to offer health benefits. But the reality that has taken hold over the years is far from that ideal. What we have now is a system in which insurers in their capacity as third-party administrators (TPAs) — the middlemen hired by employers to manage health benefits for their workers and dependents—are the real winners. One could argue that TPAs have become the biggest beneficiaries of this law, collecting billions in fees from employers while avoiding accountability. These companies are focused not on controlling health care costs in a way that ensures access to necessary care, but on maximizing their bottom lines by erecting barriers to care and systematically reducing the value of health benefits for workers.

One of the most concerning aspects of ERISA is how it allows TPAs to avoid meaningful oversight and escape legal accountability for wrongfully denied care and claims. As the law has been amended and interpreted over the years, it has allowed TPA to escape accountability in the courts, state courts in particular. That’s because ERISA preempts state laws designed to protect consumers.

If your employer-sponsored health plan refuses to cover a life-saving treatment, your options for recourse are extremely limited under ERISA. You can file an appeal, but if that fails, your ability to sue is often restricted to getting the cost of the denied treatment reimbursed, with no punitive damages and no compensation for the harm insurers acting as TPAs caused by delaying or denying care.

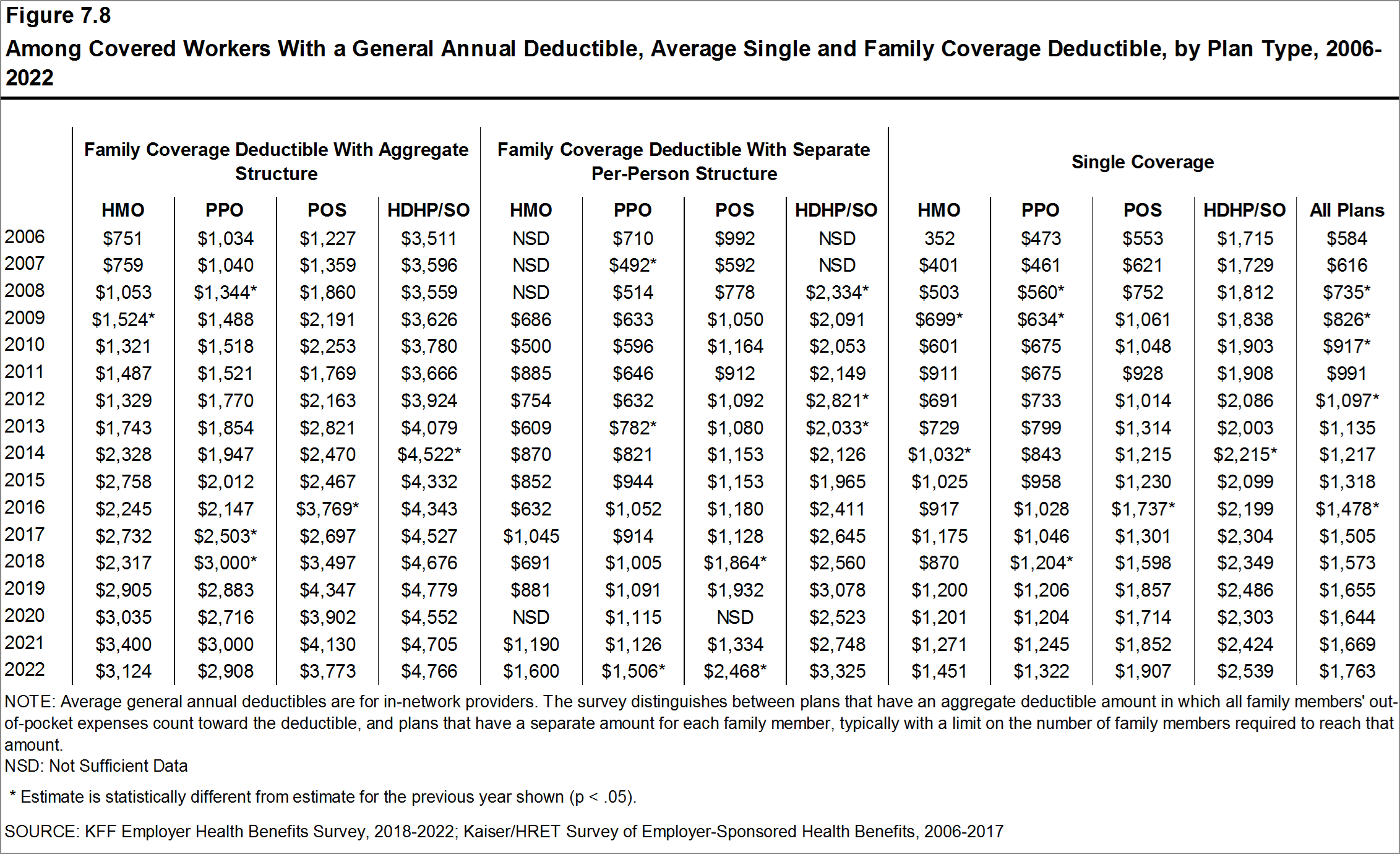

The result? Big insurers are making billions in profits every year while workers and their families are paying more for less coverage, with average deductibles now over $1,700 per year, and millions burdened with medical debt despite having employer-sponsored insurance.

{kind=link}

I’ve heard from patients who feel utterly defeated when their claims are denied. Many don’t even attempt to appeal because they believe the system is rigged against them. And they’re not wrong. But studies show that of the few who do file appeals, more than half of the denials are overturned. That means a significant portion of these denials were unjustified from the start, but insurers count on most people not fighting back. This is a glaring example of how the current system is failing to protect employees’ rights under ERISA.

Earlier this month I had the opportunity to testify before the Department of Labor’s Advisory Council on Employee Welfare and Pension Benefit Plans on behalf of my non-profit the Center for Health & Democracy. I told the council:

The insurers and TPAs have continued to consolidate, both vertically and horizontally, to the point that they have become some of the largest and most profitable corporations in the country. UnitedHealth Group and CVS/Aetna are now the fifth and sixth largest companies on the Fortune 500 list of American companies. Cigna, Elevance and other for-profit insurers are not far down the list. Last year, the seven largest publicly traded health insurers made a record $70.7 billion in profits from the money employees and employers pay them to ensure they have health care.

You can read my submitted written testimony below:

What’s needed now is clear: America’s workers need a damn break. Insurers must be required to make appeal processes and coverage criteria public. ERISA should mandate that all denial and appeal data be easily accessible, enabling independent oversight and analysis. Big health insurers, like the ones I used to work for, should face penalties when they fail to provide necessary documents or don’t adhere to legally mandated review timelines. We also need to enforce existing laws, ensuring that insurers cannot hide behind the complexity of the system to deny people the care they need.

ERISA was intended to be a safeguard for employees, but in its current state, it’s all too often doing the opposite. To truly protect workers and their families, it’s time to fix ERISA, stripping away the layers of complexity and opacity that have made it a tool for corporate gain rather than employee welfare. We need a system that works for the people, not the profiteers. Only then will ERISA fulfill the promise it made fifty years ago.

Perhaps it would be good to bring patients with you when you testify. I would be keen to do it.

After reading your attachment, it seems like there is a lot of work to do on this topic. And it is well overdue.

I sincerely wonder how to get it the attention that it needs.